by Tom Zachystal, President and founder of IAM Advisors, specialists in investment management and financial planning for Americans abroad. Click here to book a no-obligation consultation today.

For US citizens, living abroad causes complications in your investment strategy. While your overall goals usually stay the same – retirement, flexibility, family security – the environment around those goals changes.

Most investing issues for expats stem from a handful of reasons. Brokerage account access can become uncertain, product rules differ by country, currency movements can affect your spending power, and many US expats are subject to both local and US reporting requirements. Add all these together, and the landscape becomes challenging.

In this article, we’ll walk you through some of the investing considerations that matter most for Americans living abroad, to provide clarity and help you stay on track for your long-term goals as an American investor living abroad.

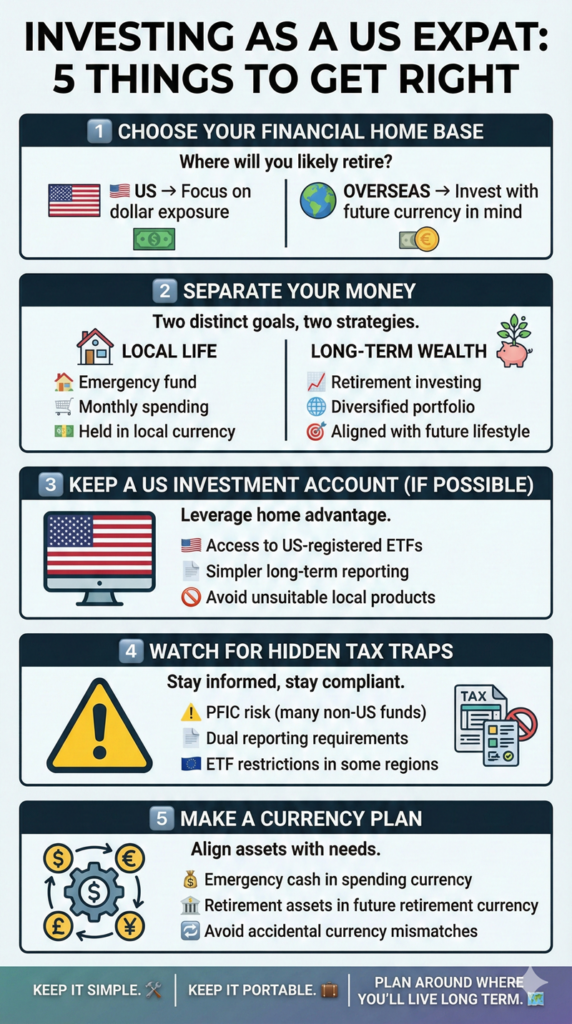

Consider Where Is Your “Financial Home Base”

Every expat benefits from a clear picture of where money lives and why.

It can help to choose a financial home base. This doesn’t need to match your passport or your current address – it should normally reflect where you expect to settle long term or spend most of your later years. This means that a short overseas assignment calls for a different investment strategy than a permanent move abroad.

If you expect to return to the US, keeping your plan anchored to the dollar often makes sense. If you expect to stay overseas long term, it can make more sense for your investments to reflect the currency and markets tied to your future spending.

It can also help to separate your money into two functional buckets:

- Local spending money: cash flow, bills, and near-term goals held in the currency you use day to day.

- Long-term wealth: diversified investments designed to support retirement and multi-decade objectives.

This simple split reduces pressure and prevents you from dipping into long-term investments to fund day to day expenses.

Keep a US-Based Investment Account if You Can

For many Americans abroad, a US brokerage account remains the backbone of their investment strategy.

US markets offer depth, liquidity, and a wide range of low-cost investment options. They also reduce the risk of buying products that look familiar locally but create problems later for US citizens.

There is a practical reason this matters. Many expats run into trouble after investing through local platforms that sell products unsuitable for Americans. A US-based account naturally steers you toward US-registered funds and Exchange-Traded Funds (ETFs), which often simplify reporting and long-term planning.

The challenge is access. Some US financial institutions restrict or close accounts for clients who live abroad due to US compliance rules relating to non-resident clients.

A few steps can help reduce friction:

- Keep your broker updated on your residency status and contact details.

- Maintain reliable US contact methods for security and verification.

- Consolidate accounts if you have multiple small relationships that increase administrative risk.

If a custodian does not support your country of residence, an expat-specialist investment advisor can help you identify platforms and brokers who are happy to work with expats.

Understand Local Product Rules That Block “Easy” ETF Investing

Living outside the US can complicate something as simple as buying an Exchange-Traded Fund (ETF).

In all the countries in the EU for example, local regulations limit access to US-domiciled ETFs for retail investors.

This creates an expat investing dilemma. US ETFs often align well with US reporting and long-term planning, while local funds may appear convenient but introduce new complexity for Americans.

You can still build a diversified portfolio despite these constraints, but the solution depends on structure and where you live. Seek advice from an expat financial advisor to discuss your options based on your situation.

Avoid PFICS and Other Hidden “Bad Wrappers”

One of the most common expat investing mistakes involves owning the wrong type of overseas investment.

Many non-US mutual funds, ETFs, unit trusts, and pooled products fall under the IRS Passive Foreign Investment Company regime. PFIC treatment can turn an otherwise ordinary foreign investment into a tax and compliance headache.

The paperwork alone can outweigh any potential benefit. For many Americans abroad, the issue is not performance, it is the administrative burden.

A practical rule of thumb helps:

- Prefer US-registered ETFs and mutual funds when access allows.

- Treat locally offered mutual funds and packaged investments with caution.

- Ask clear questions about where a product is domiciled and how it is classified for US purposes.

PFICs can also lead to large unexpected US tax bills.

Build a Currency Plan

Currency exposure plays a larger role once you live and spend abroad.

It is entirely possible to earn solid investment returns but lose them again due to exchange rate moves. Without a plan, currency risk can dominate outcomes.

A good approach is to link assets to future spending. If you expect to retire in Europe, meaningful exposure to euros makes sense. If retirement likely happens in the US, dollar exposure deserves priority.

You do not need to forecast currencies. You need to reduce mismatches.

A few practical principles go a long way:

- Hold your emergency fund in the currency you use for monthly expenses.

- Align retirement assets with the currency you expect to spend in retirement.

- Use broad global investments with intentional, not accidental, currency exposure.

Many expats focus too much on the currency of their salary. Your future lifestyle matters more.

Treat Foreign Pensions and Employer Plans as a Separate Project

Foreign pensions and mandatory employer plans often provide valuable benefits, including employer contributions and local tax incentives. They can also introduce uncertainty for Americans, especially when US tax treatment differs from local rules.

Rather than forcing these plans into a US framework, step back and assess them on their own terms.

Four questions can help bring clarity:

- What is the real local benefit, including employer contributions?

- How portable is the plan if you leave the country?

- How does it fit into your broader retirement picture?

- Does the US respect the tax advantages (this will relate to the particular tax treaty between the US and the country where you live)?

If participation is mandatory, think of the plan as separate from your long-term investment strategy, and make sure you understand the US tax treatment of local plans. Then build flexible savings around it using accounts that remain portable across borders.

Keep Retirement Investing Simple and Portable

Americans abroad often accumulate accounts in multiple countries. Over time, this can turn into an administrative burden.

A few principles help keep retirement investing manageable:

- Capture employer matches when available.

- Avoid overexposure to a single employer or local market.

- Consolidate accounts when it improves clarity and reduces costs.

- Maintain an investment policy that still works after your next move.

Be mindful of timing. Some US providers make it difficult to open new accounts once you hold a foreign address. Planning ahead can preserve options.

A Practical Expat Investing Checklist

A US expat specialist investment advisor can help you evolve your investments for life abroad, including for both US and foreign compliance and tax optimization:

- Confirm your US brokerage can support your country of residence and your address. If not, change to one that does.

- Confirm which US investment products you can buy under local rules, especially if you live in the EU/EEA.

- Screen any non-US fund or “wrapper” product for PFIC risk and reporting burden. Also be mindful of the fees associated with such products because they tend to be significantly higher than in the USA and may outweigh any benefits.

- Create a one-page currency plan tied to your expected retirement location.

- Decide where you keep emergency cash and how you move money across borders.

- Document beneficiaries, powers of attorney, and where key account logins live.

When You Should Bring In an Expat-Focused Advisor

If you only have a US 401(k) and a checking account abroad, you probably won’t need help. If you have US brokerage accounts and want to keep investing, or foreign pensions, a spouse of another nationality, property or business interests abroad however, you will almost certainly benefit from advice.

Look for someone who works with Americans abroad and designs portfolios around:

- Custody access for non-US residents.

- Product constraints like PRIIPs.

- Currency exposure tied to your life plan.

- Clean, repeatable systems that survive country changes.

When investing while living abroad, you should aim to take into account cross-border compliance and tax optimization while focusing on your long-term plans and goals. Some restructuring or strategy evolution may be required, but with specialist cross-border advice, your life overseas shouldn’t impede on your ability to invest and grow your wealth.

If you’re a US expat looking for clear, expert financial guidance, speak directly with Tom Zachystal, President of IAM. With over 20 years’ experience helping Americans abroad, Tom offers personalised investment management and cross-border financial planning tailored to your situation. Book your free, no-obligation consultation today and take the first step toward protecting and growing your future — with complete privacy guaranteed.